INDUSTRY UPDATE: Management Consulting – December 2022

Management Consulting Introduction

When researching the management consulting industry, the first aspect one is likely to notice is its amorphous contours; as one source puts it:

“Despite the relatively mature state of the market, the large variety of services (industries, functional areas, market/region focus) that span the consulting industry imply that there is no clear-cut consensus on how the market should be defined. Representative bodies (e.g. the MCA in the UK) and analyst firms (e.g. ALM Intelligence, Gartner, etc) all use different market definitions, and as a result the estimates for the size of the consulting market differ substantially, ranging from just over $100 billion up to $280 billion.” [See source.]

Consequently, there are a variety of estimates of how large the market is and how fast it is growing. Readers will find one set of data below that seems widely accepted.

The US market, presumably the largest in the world, has grown explosively in recent years:

“In 2022, the management consulting services industry in the United States generated a total of approximately 329 billion U.S. dollars. Between 2012 and 2022, the management consulting services industry grew exponentially and was worth 100 billion U.S. dollars more in 2022 as in 2012.” [See source.]

The European market seems to have recovered considerably from the Covid-induced contraction:

“The Management Consultants industry’s revenue is expected to increase at a compound annual rate of 2.8% over the five years to 2022 to total €225.5 billion. Following a steep decline over 2020, business confidence is expected to grow over the two years through 2022, which is anticipated to support demand and revenue growth. Industry revenue is forecast to rise by 2.5% in 2022…” [See source.]

The Middle East is also a hotbed of activity:

“From advising Saudi Arabia on the key pillars of its Vision 2030 or helping the United Arab Emirates with advancing its travel and tourism hotspot strategy, to supporting the Lebanese government with its mammoth task of saving its economy from the brink of collapse, strategy consultants are in high need across the Middle East and Arabic part of North Africa (MENA).

The region is buzzing with change, and strategy consultants are working on some of the most pressing and high impact challenges and transformations in the private and public sector.” [See source.]

Looking ahead…

The global management consulting industry “is anticipated to grow by $814.6 billion by 2031, at a CAGR of 10.6% during the prediction period.” [See source.]

While the priorities will likely vary by geographic market and industry, some broad areas of focus for the management consulting industry as highlighted by LinkedIn (See source) may well include the following:

- Ongoing digitalization

- The Impact of Law on Business

- Target Market (As the management consulting industry expands, it continues to divide into two market segments: a commoditized, low-cost sector and a high-value, specialized consulting sector)

- Digital Integration (…consultants will build thorough digital strategies and reimagine the current business and operational models in 2023.)

- Fail Fast Methodology (…an agile development mindset that makes use of the idea of “failing quickly.” )

- Recruiting New Talent (The emphasis on skill sets in hiring fresh personnel is continuing to replace the conventional top-tier universities.)

- Multi-Sourcing Mode (…large generalist companies collaborating with smaller niche specialists; management consulting companies teaming up with consultants from outside the sector; and consultancies teaming up with academic institutions, digital agencies, and technology firms.)

- Crowd-Sourced Talent (…a disruptive business model that enables clients to hire piecemeal from specialized companies or independent contractors…)

Beyond these intriguing subjects, leveraging artificial intelligence, the future of work, and numerous aspects of green energy as well as environmental sustainability will occupy business management in the coming years and therefore remain promising territory for management consulting.

The Executive Market: Management Consulting

Readers may have heard that crisis breeds opportunity. It certainly also breeds management consultants—at least based on LinkedIn data.

Executives as we define them (see Editor’s Note) who claim Management Consulting as their primary industry on LinkedIn number some 284,000 in our target geographies*—having grown 3% versus the prior year and implying some 17,000 executive opportunities (job changes plus industry growth) over the last 12 months. This population is predominantly male (75%), exhibits on average a “high” hiring demand per LinkedIn, and an average tenure of 3.9 years.

Approximately 150,000 of these positions are located in the EU, UK, and Middle East, a market that also grew by 3% YOY where Paris, London, Munich, the UAE, and Madrid occupy the top locations. This market has a somewhat lower female share (22%) and shorter tenure (3.8 years). In the US, some 134,000 executives claim this as their main field of endeavor, up 3% YOY, with a slightly higher female share (29%) and longer tenure (4.1 years).

*While the Barrett Group serves clients all over the globe, the majority of our clients are in the US, Europe, the UK, and the Middle East.

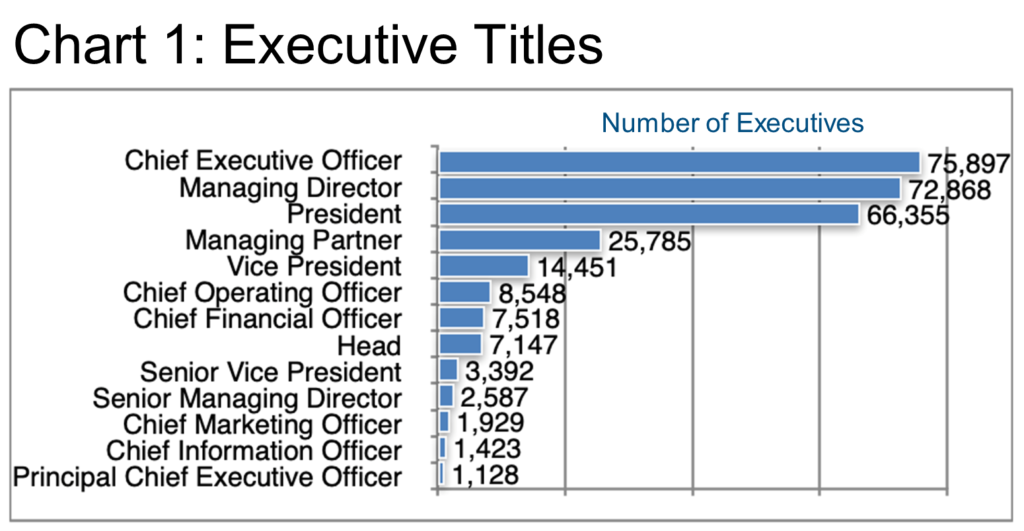

Chart 1 describes the title landscape that seems heavily skewed toward the top of the organization implying a relatively small average company size. As we will see in subsequent charts, the industry is dominated by a few larger concerns and has a long list of smaller, presumably specialized firms in its roster.

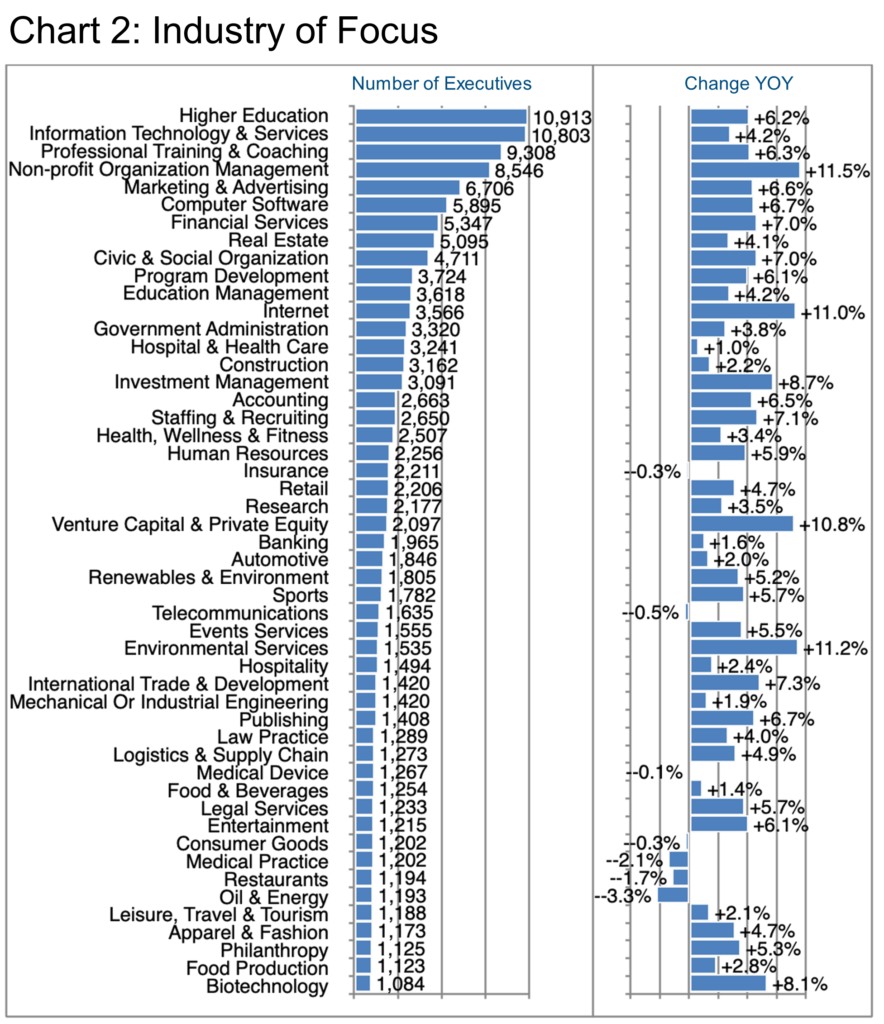

In Chart 2 we examine the industrial focus of this executive population. As far as relative size is concerned, it will surprise no one to see Information Technology & Services high on the list, but it may well surprise readers to see Higher Education at the top of the chart, or Professional Training & Coaching, and Non-profit Organization Management in the top five, the latter showing the highest growth of any industry focus.

While the growth YOY is visible in Chart 2, LinkedIn also distinguishes some tracks as exhibiting higher or lower “hiring demand” irrespective of growth, meaning even if the growth is relatively low there could be high attrition or numerous executives changing industries and thus creating vacancies.

Here are a few highlights:

While any given management consultant may be a specialist in a limited number of specific areas, it is not surprising that, taken as a whole population, management consultants cover most key business areas as shown in Chart 3.

It seems to us in fact that the bulk of management consultants per this analysis tends to be generalists (e.g., Business Planning, New Business Development, etc.) versus farther down in the ranking more specialist activities such as Outsourcing or Due Diligence. This becomes a relevant consideration, especially for those who might like to migrate into the management consulting industry and wonder about the transferability of their skills and experience.

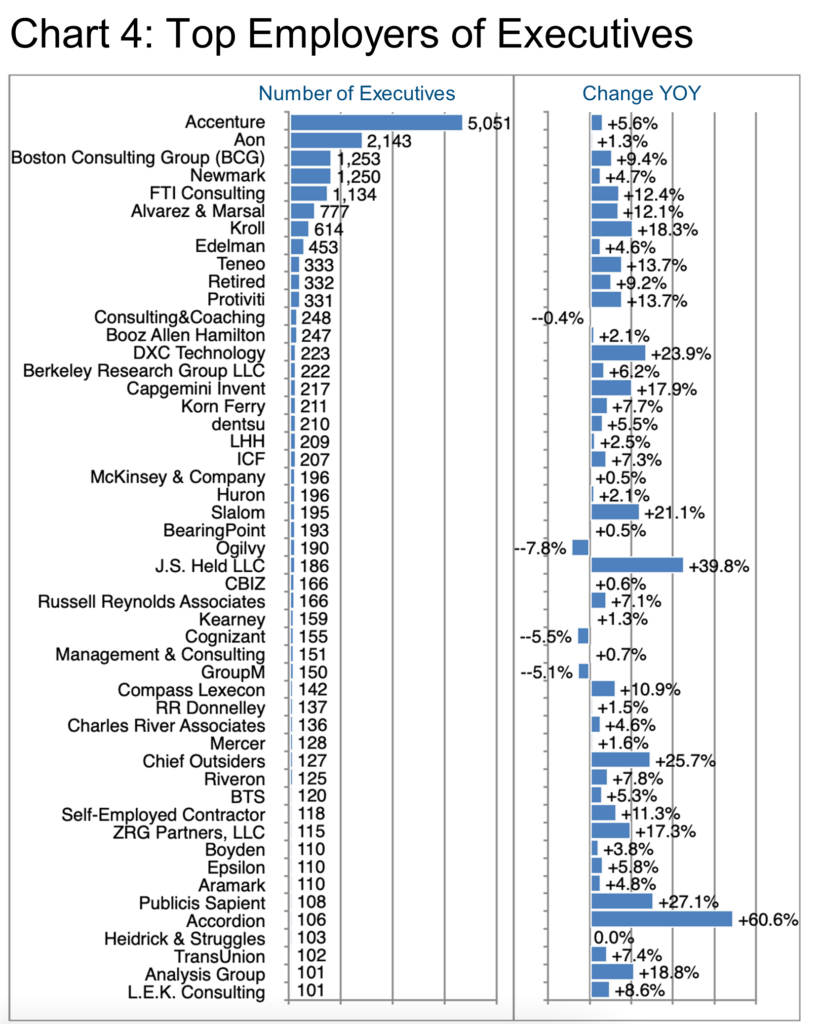

Chart 4 explains our comment about relative concentration in the industry with Accenture employing more than twice as many executives as their next largest competitor. The numbers decline rapidly thereafter as the size of the organization declines. This is consistent with the title architecture we highlighted in Chart 1.

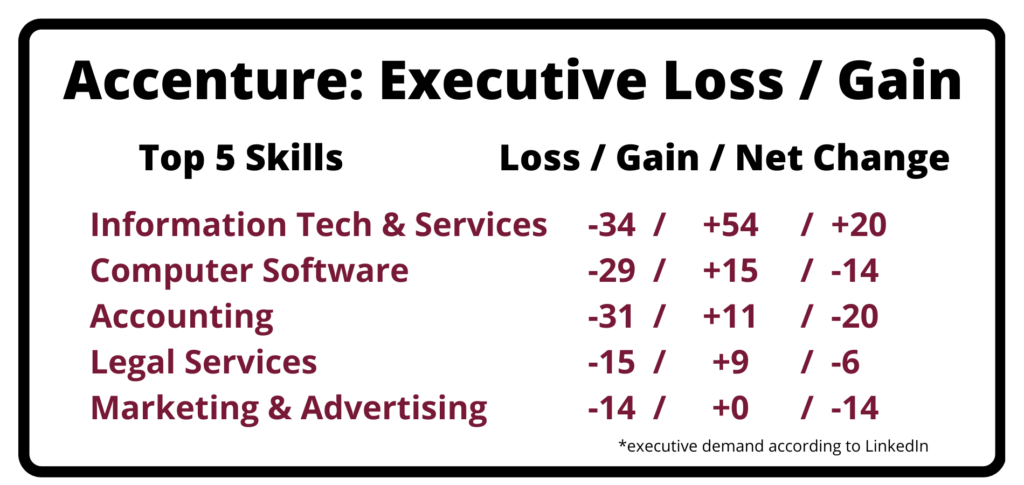

Of course Barrett Group clients have access to very specific information. It includes industry, location, company, and even individual executive data.

However, for the purposes of this Update let us examine the largest player in more detail. During the past year, Accenture gained or lost executives for these top five skills (among many others):

Geographically, the company hired executives broadly: +6% in New York, +4% in London, +10% in San Francisco, and +5% in Paris, to name a few selected locations—all of them above the industry average. According to LinkedIn, Accenture actually added more than 52,000 total staff in the past year, hiring from Deloitte, Cognizant, Capgemini, Infosys, IBM, Wipro, EY, Genpact, and HCL Tech.

For comparison, take Boston Consulting Group (BCG) whose executive ranks swelled by more than 9% YOY. They also hired broadly from competitors such as Deloitte, Accenture, EY, Bain & Company, McKinsey & Company, PwC, Kearney, but also big tech, e.g., Amazon and Google. Geographically, BCG added staff in New York, Delhi, Boston, London, Paris, Munich, Chicago, Atlanta, Washington DC, and Milan.

To explain some of the most extreme growth in Chart 4, J.S. Held LLC grew by more than 39% through its October 2022 acquisition of TBG Security, a cyber security consultancy (and no relation of the Barrett Group). Another fast grower, Accordion, received a significant investment in 2022 and has hired fairly continuously from Mackinac Partners and Grant Thornton LLP (USA) as well as from most of the major management consulting firms.

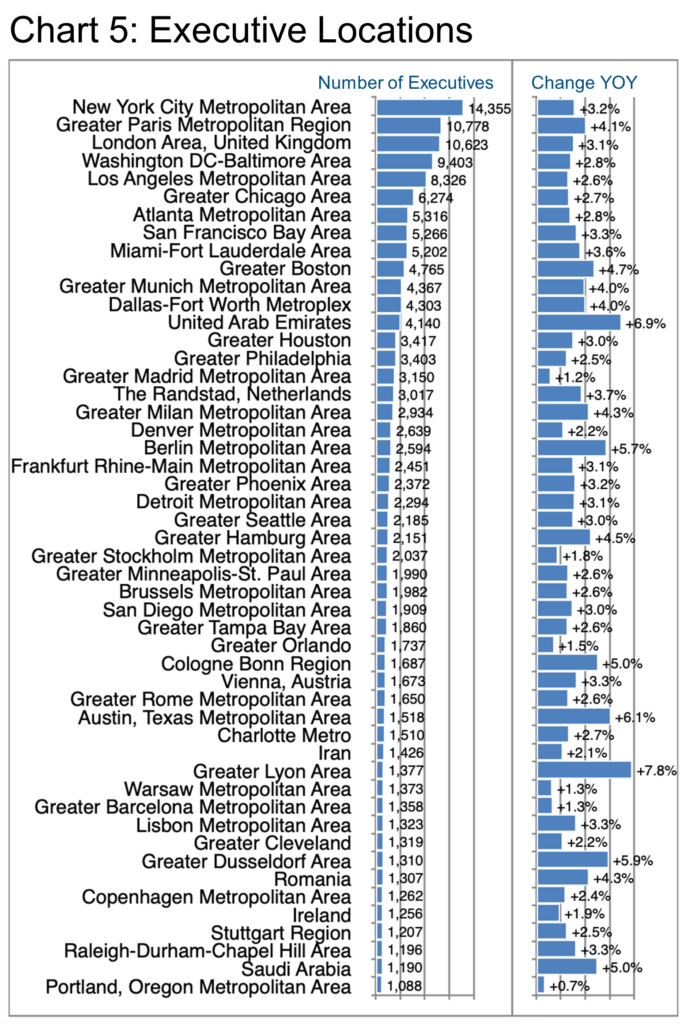

Chart 5 opens up the subject of location (place of employment, not necessarily working location). That New York is number one is fairly usual. Nor is it a big revelation that Los Angeles and Washington DC should appear in the top five, however, that London and Paris occupy second and third place is highly unusual at least compared to other industries we have studied.

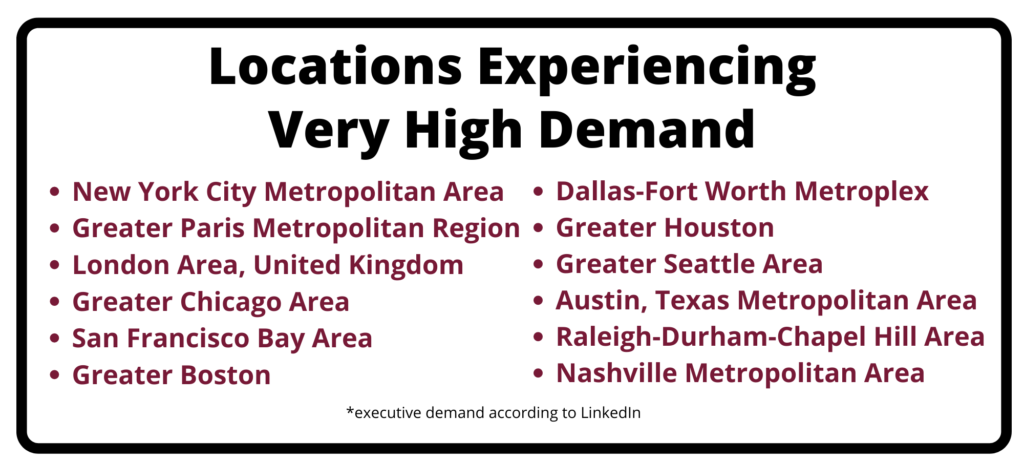

From a growth point of view, the UAE (+6.9%) and Saudi Arabia (+5%) stand out, but so do Lyon (+7.8%), Austin (+6.1%), Dusseldorf (+5.9%), Berlin, (+5.7%), and Bonn (+5%). As we have mentioned before, a high hiring demand may exist in a market or a profession regardless of the growth rate. These locations are all rated as having a “very high hiring demand” by LinkedIn:

Other locations such as Hamburg, Bonn, and even the UAE, having grown relatively fast in the recent year now rank as having low hiring demand. Most likely this reveals a period of recovery perhaps from the pandemic that may now have normalized.

The Barrett Group helps clients reposition in any market by reviewing their aspirations to come up with a holistic professional target encompassing income requirements, location, industry, role, and especially quality of life.

Female Executive Focus

Given the relatively low female executive share in this industry (25%) it might be encouraging to focus on some of the areas where female executives are making more progress.

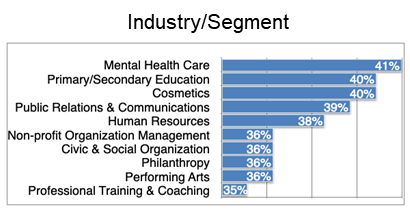

| The top chart in this box focuses on the industrial segments with the highest female executive shares. |  |

|

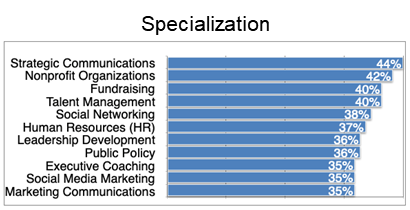

| The second chart highlights the executive specializations with the highest female executive shares. |  |

|

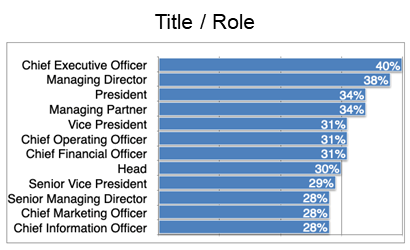

| Per the third chart in this block, that 40% of the CEOs in this industry should be female seems quite refreshing. In fact all of the listed executive titles exceed the average female executive share of the industry. |  |

|

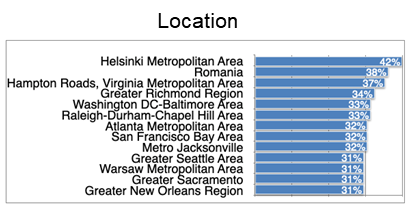

| In the last chart in this block we look at the locations with the highest share of female executives. The US may take some time to challenge Finland and Romania but many locations are making progress. [See Industry Update: Female Executives.] |  |

Peter Irish, CEO

The Barrett Group

Click here for a printable version of Industry Update – Management Consulting 2022

Editor’s Note:

In this particular Update “executives” will generally refer to the Vice President, Senior Vice President, Chief Operating Officer, Chief Financial Officer, Managing Director, Chief Executive Officer, Chief Human Resources Officer, Chief Marketing Officer, Chief Information Officer, Managing Partner, General Counsel, Head, and President titles. Unless otherwise noted, the data in this Update will largely come from LinkedIn and represents a snapshot of the market as it was at the time of the research.

Is LinkedIn truly representative? Here’s a little data: LinkedIn has more than 800 million users. (See source) It is by far the largest and most robust business database in the world, now in its 19th year. LinkedIn defines the year-over-year change (YOY Change) as the change in the number of professionals divided by the count as of last year and “attrition” as the departures in the last 12 months divided by the average headcount over the last year.